Third FOR 5583 Internal Seminar

Online via Zoom

February 9, 2026

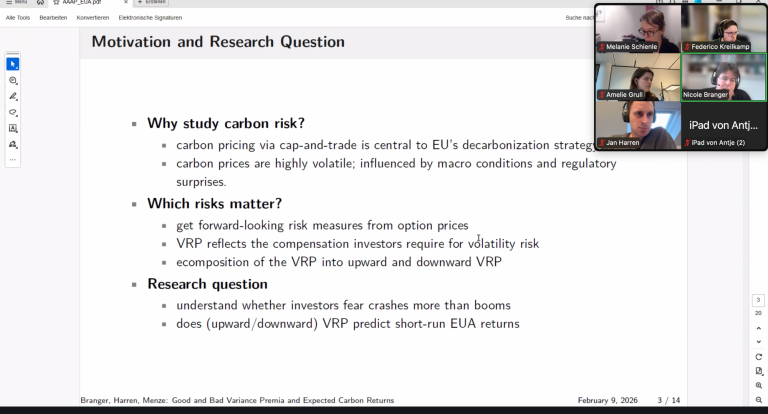

On February 9, our online seminar series continued with a stimulating talk by Prof. Nicole Branger titled “Good and Bad Variance Premia and Expected Carbon Returns”.

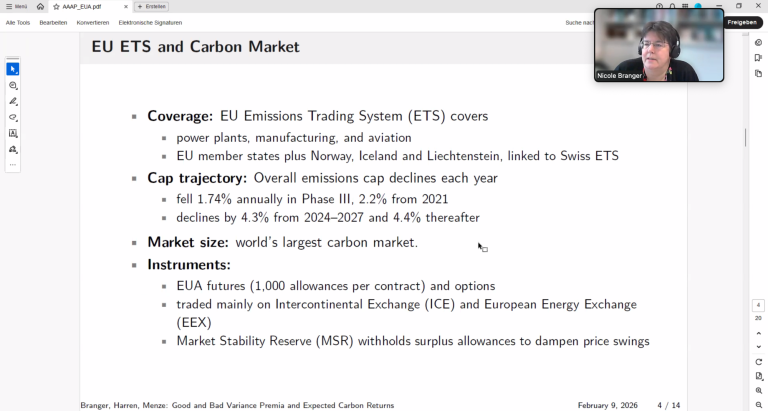

In this ongoing joint project, Prof. Branger and her co-authors adapt the idea of decomposing “good” (upside) and “bad” (downside) variance premia to the context of carbon prices. The presentation explored how separating upside and downside variance in carbon markets can shed light on expected carbon returns. Preliminary results suggest that “good” and “bad” variance premia in carbon prices have distinct predictive power for future returns and may help disentangle different channels of climate and policy risk.

We were also pleased to have Prof. Steven Vanduffel (currently visiting Institute of Insurance Science - Ulm University), Jan Harren and Stefan Menze in attendance. Their presence contributed to an especially lively and technically rich discussion.

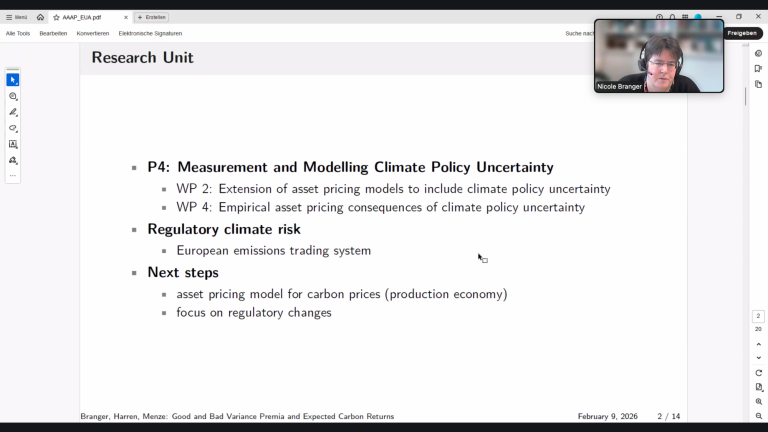

The session once again underscored the breadth and depth of research within our research unit “Asset Allocation and Asset Pricing under Regulatory Uncertainty.”